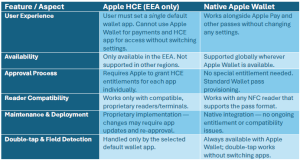

While Apple has enabled Host Card Emulation (HCE) support for third party apps in the EEA, there are significant differences and limitations compared to using the native Apple Wallet:

1. Default Wallet Selection and User Experience

- With HCE, the user must select a single default wallet app that handles double-tap on the side button and NFC field detection – weather it should be the native Wallet or third-party app.

- This creates an inconsistent experience for users who want to use Apple Wallet for payments but a third-party HCE app for access control.

2. Regional Limitation

- Apple’s HCE capability is currently available only in the EEA region. Outside of this area, the feature is unavailable, making global deployments inconsistent.

3. App-Specific Entitlement Approval

- The HCE entitlement is not granted by default. Each app requires separate approval from Apple, which may add uncertainty and delays to deployment.

4. Proprietary and Reader-Dependent

- An HCE app is a proprietary solution tied to specific protocols and compatible readers/terminals. This means it will not interoperate with standard NFC use cases over ECP protocol unless explicitly supported.

Why the native Apple Wallet provisioning is preferable

- Passes are stored in the system’s built-in Wallet, which is always available, globally supported, and does not require the user to set a default wallet app.

- The double-tap and NFC detection work seamlessly alongside Apple Pay and other wallet passes.

- Deployment is simpler — no special entitlements or region-specific limitations.

- Works with any compatible NFC reader without requiring proprietary terminal firmware.

In short, while HCE on iOS is a welcome regulatory-driven change, it adds friction for users and operational complexity for deployers. The native wallet solution offers a more seamless, universal, and user-friendly experience.